With prices on the rise in nearly every area of life, it’s natural to wonder how the housing market is holding up—especially here in the Inland Empire. Some homeowners and buyers in San Bernardino and Riverside counties are concerned that rising living costs might lead to more missed mortgage payments and possibly a spike in foreclosures. And yes, national data shows a slight uptick in foreclosure filings. But here’s why that shouldn’t set off alarm bells—especially in our local market.

This Isn’t Like 2008

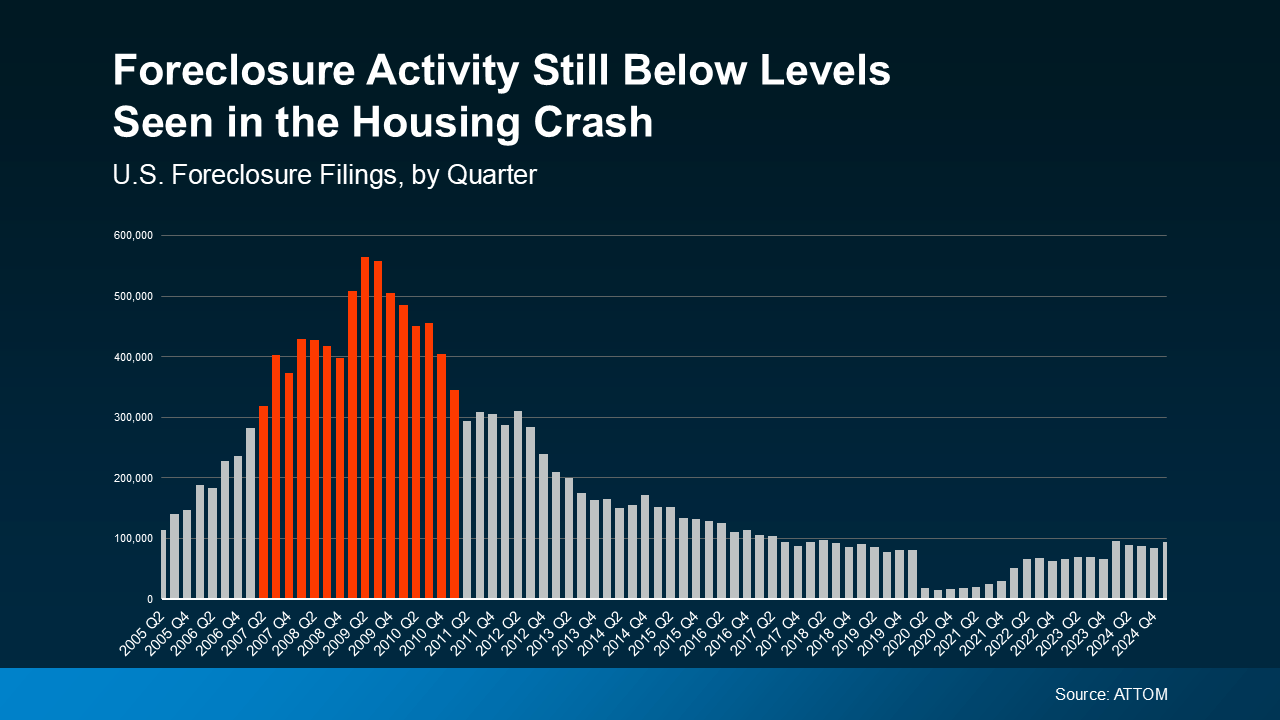

While foreclosure activity did tick up slightly in the most recent ATTOM report, numbers are still well below historical norms—and nowhere near the crisis levels we saw in 2008. When you zoom out and view the long-term trend, the difference is clear.

During the last housing crash, loose lending practices led many homeowners into loans they couldn’t afford. That triggered a flood of foreclosures, oversupply in the market, and steep price declines—including right here in the Inland Empire, which was one of the hardest-hit regions in California.

Today is very different. Lending standards are much stricter, and the majority of homeowners are in a healthier financial position. In fact, foreclosure filings remain well below pre-pandemic norms in Riverside and San Bernardino counties, even with today’s economic pressures.

It’s also important to note that 2020 and 2021 were unusually low due to federal foreclosure moratoriums, which gave homeowners relief during the pandemic. That’s why recent numbers might look like a jump, when in fact, we’re still trending below more typical levels—like those seen between 2017 and 2019.

Foreclosures Are Rare, and Equity Is a Big Reason Why

One reason we’re not seeing a foreclosure wave in the Inland Empire is because local homeowners have built significant equity over the past few years. Our region saw double-digit home price appreciation during the pandemic housing boom, and even though price growth has slowed, most owners still have a strong equity cushion.

As Rob Barber, CEO at ATTOM, puts it:

“While levels remain below historical averages, the quarterly growth suggests that some homeowners may be starting to feel the pressure of ongoing economic challenges. However, strong home equity positions in many markets continue to help buffer against a more significant spike . . .”

That’s especially true in our local market. Homeowners here who may be facing temporary financial difficulty are often able to sell their home and walk away with equity rather than going through foreclosure. That’s a major difference from 2008, when many Inland Empire residents were underwater on their mortgages and had few, if any, options.

Rick Sharga, Founder and CEO of CJ Patrick Company, adds:

“ . . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

Bottom Line

Even with a slight uptick in foreclosure activity, the numbers in San Bernardino and Riverside counties are nowhere near the crisis levels of the past. Most homeowners here still have solid equity and better financial footing than in previous downturns.

If you’re a homeowner in the Inland Empire facing financial hardship, reach out to your mortgage provider to discuss your options. In many cases, selling your home or negotiating new terms could help you avoid foreclosure altogether.